Most business buyers don’t realize the IRS requires two separate filings the day a deal closes — one from the buyer and one from the seller — each reporting how the purchase price was divided among asset categories. Whether you’re the buyer inheriting a depreciation schedule or the seller managing capital gain exposure, IRS Form 8594 — the Asset Acquisition Statement Under Section 1060 — governs how that division is reported. Getting this allocation right matters enormously: it determines whether gains are taxed at ordinary income rates or the lower capital gains rate, and it shapes how quickly the buyer can recover the purchase price through depreciation and amortization.

🧐Don’t let your business sale turn into an IRS follow-up. Have Simplicity Financial align your allocation.

What’s Form 8594?

IRS Form 8594 is the tax form both buyers and sellers must file when a business is sold as a collection of assets rather than as a transfer of stock or ownership shares. Formally titled the Form 8594 Asset Acquisition Statement, it requires both parties to report how the total purchase price is allocated across seven predefined asset classes established under Section 1060 of the Internal Revenue Code.

The legal foundation is IRC Section 1060, which mandates the residual allocation method whenever a group of assets constituting a trade or business is transferred. The IRS requires both the buyer and the seller to file tax form 8594 independently, each attaching it to their own federal income tax return for the year the sale occurred.

A key distinction: what is Form 8594 not used for? It does not apply to stock sales, where the buyer acquires ownership shares rather than individual assets. In a pure stock sale, the company’s assets and liabilities transfer with the entity itself, and no asset-by-asset allocation is required. The form is specifically triggered when assets — not shares — are the subject of the transaction.

When is Form 8594 Required?

Form 8594 is required when two conditions are both met: a group of assets constituting a trade or business is transferred, and the buyer’s tax basis in those assets is determined wholly by the amount paid. If both conditions apply, Form 8594 filing is mandatory for both buyer and seller — no exceptions for transaction size or entity type.

The form must be filed for the tax year in which the sale closes. If the purchase price allocation changes after the initial filing — due to earnout payments, post-closing adjustments, or escrow releases — an amended Form 8594 must be filed in the year the change takes effect. Form 8594 requirements also extend to reporting any inconsistency between what the buyer and seller report.

Per the IRS Form 8594 instructions page, both parties must independently complete and attach the form to their federal return, whether that’s a Form 1040, 1120, 1065, or 1120-S.

Does Form 8594 Apply to Stock Sales?

Generally, no. A pure stock purchase does not trigger Form 8594. The buyer steps into the seller’s shoes as a shareholder, and no asset-level allocation is needed.

The notable exception is a Section 338(h)(10) election, which — when made jointly by buyer and seller — causes the IRS to treat a qualifying stock purchase as a taxable asset sale, requiring Form 8594 even though shares physically changed hands.

Understanding the 7 Asset Classes Used on Form 8594

The seven asset classes on the Form 8594 Asset Acquisition Statement are central to the entire filing. Under the residual method required for tax accounting for acquisitions, purchase price flows through seven defined asset classes in strict order. The table below summarizes each class, common examples, and the tax treatment that makes classification so consequential:

| Class | Asset Type | Examples | Tax Treatment |

| Class I | Cash and general deposit accounts | Checking accounts, petty cash | Allocated at face value; no gain or loss |

| Class II | Actively traded personal property | CDs, U.S. government securities, foreign currency | Ordinary income or capital gain depending on asset |

| Class III | Accounts receivable and similar assets | Customer receivables, mortgages | Ordinary income on collection |

| Class IV | Inventory | Products held for sale, raw materials | Ordinary income upon sale |

| Class V | All other tangible and intangible assets | Equipment, furniture, vehicles | Depreciation recovered as ordinary income; remainder as capital gain |

| Class VI | Section 197 intangibles (except goodwill) | Non-compete agreements, customer lists, patents | Amortized over 15 years; gain on sale is ordinary income |

| Class VII | Goodwill and going concern value | Brand reputation, uncontracted customer relationships | Amortized over 15 years by buyer; capital gain for seller |

Why does the classification order matter so much? The IRS requires purchase price to be allocated first to Classes I through VI at fair market value, with any remaining amount assigned to Class VII. This hierarchy means goodwill absorbs the residual — and for many service businesses, that residual is the largest single number.

The buyer-seller tension is real: buyers prefer more allocation to Class V assets like equipment, depreciable over 5 to 7 years. Sellers prefer goodwill (Class VII) because it generates capital gain rather than ordinary income. Most small business acquisitions concentrate value in Classes V through VII, making negotiation over these three classes a meaningful deal point.

How to Fill Out Form 8594: Step-by-Step Instructions

Before completing the form, review other tax forms for acquisitions that may also apply to your transaction, such as those triggered by equity compensation or installment sales.

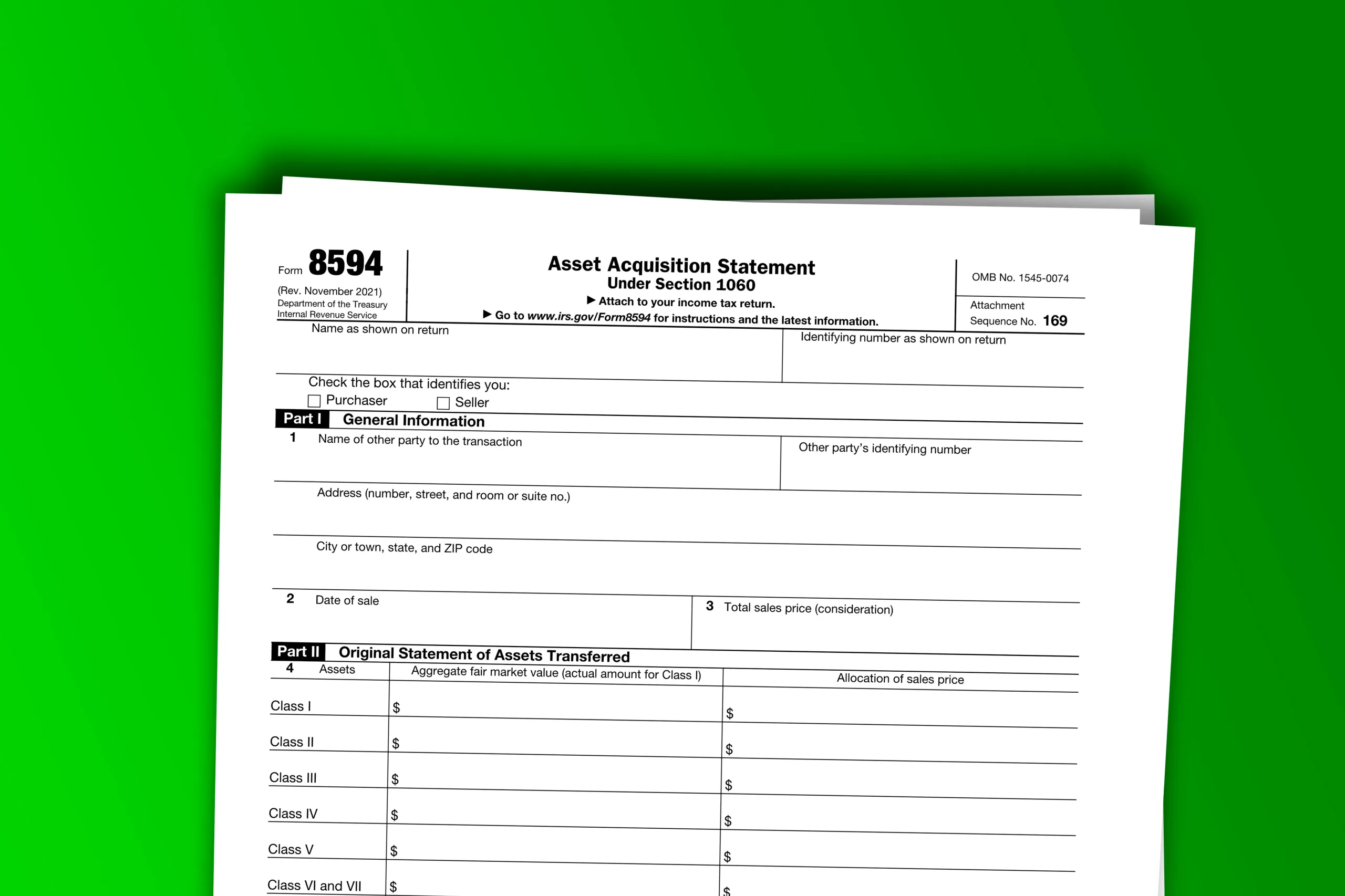

Part I: General Information

Part I captures identifying details of the transaction. Enter the name and Employer Identification Number (or Social Security Number) of the other party — the buyer enters the seller’s information, and vice versa. Record the date of sale and the total consideration paid, which includes cash, assumed liabilities, and the fair market value of any other property transferred. Check the box indicating whether you are the buyer or the seller.

Part II: Original Statement of Assets Transferred

Part II is where the allocation work happens. For each of the seven asset classes, enter the aggregate fair market value of assets in that class and the portion of the total purchase price allocated to it. Per the official IRS Form 8594 instructions (IRS.gov), the residual method dictates the sequence: allocate to Classes I through VI first at fair market value, then assign the remainder to Class VII. Buyer and seller should use consistent allocations; if they differ, both must disclose the inconsistency.

Part III: Supplemental Statement

Part III applies when the original purchase price allocation changes after the initial filing. Common triggers include earnout payments, indemnification adjustments, or escrow releases. When any of these occur, an amended form — following instructions Form 8594 Part III — must be filed for the tax year in which the change takes effect. Failing to file the supplemental statement is one of the more frequently overlooked compliance gaps in post-closing tax administration.

Form 8594 Example: A Real-World Business Sale Allocation

A form 8594 example makes the abstract allocation process easier to follow. Consider a buyer who purchases a small professional services firm for $500,000 in a qualifying asset sale. Here is how the purchase price might be allocated:

- Class I — $10,000 (cash in operating accounts)

- Class II — $0 (no government securities or CDs)

- Class III — $15,000 (outstanding client receivables)

- Class IV — $0 (service business; no inventory)

- Class V — $75,000 (computers, office furniture, equipment)

- Class VI — $100,000 (non-compete: $40,000; customer list: $60,000)

- Class VII — $300,000 (goodwill and going concern value)

- Total — $500,000

Note that certain asset sales — particularly those involving real property — may also require reporting 1099-S income, which interacts with how proceeds are characterized on the seller’s return.

The buyer’s preference in this Form 8594 for asset sales scenario would be to push more value into Class V equipment, depreciable over 5 to 7 years, rather than Class VII goodwill at 15-year amortization. From the seller’s side, the $300,000 Class VII goodwill allocation is advantageous precisely because it generates capital gain treatment — which is why sellers typically negotiate for higher goodwill values while buyers push back. That conflict belongs in deal negotiations, not as a surprise after closing.

What Happens When the Buyer and Seller Disagree on the Allocation?

Buyers and sellers routinely have opposing tax interests when allocating purchase price, and those conflicts don’t always resolve cleanly at closing. Form 8594 buyer and seller requirements mandate that each party file independently — but also require disclosure when those filings are inconsistent.

When buyer and seller submit different allocations without mutual agreement, both must check a box on Form 8594 acknowledging the inconsistency. The IRS can then examine both filings and recharacterize the allocations to reflect what it determines was the arm’s-length value for each asset class. The result can be additional taxes, interest, and penalties for one or both parties.

Working with professional tax preparation services experienced in business acquisitions is the most reliable way to align allocations before closing and avoid this outcome.

In our experience advising clients through business sales, unresolved allocation disputes are among the most preventable — and most damaging — post-closing surprises.

The U.S. Small Business Administration notes that thorough pre-transaction analysis — including tax structure review — is essential due diligence for any business acquisition.

Common Mistakes to Avoid When Filing Form 8594

The 8594 form trips up buyers and sellers in predictable ways, and most errors are avoidable with proper preparation. With tens of thousands of small business ownership transfers occurring annually in the U.S. (Statista), the IRS has extensive pattern data on Form 8594 errors — making accuracy more important than many filers realize.

The most common mistakes include:

- Only one party files. Both the buyer and seller must file IRS Form 8594 separately. Assuming the other party handled it is a compliance failure.

- Inconsistent allocations without disclosure. When buyer and seller report different allocations, both must disclose the inconsistency. Silently filing different numbers invites scrutiny of both parties.

- Misclassifying assets. A customer list belongs in Class VI, not Class V. A non-compete agreement is a Section 197 intangible — not equipment. Misclassification changes tax treatment and can be recharacterized on audit.

- Forgetting the amended form. If earnouts, escrow releases, or indemnification adjustments change the final purchase price, a supplemental Form 8594 is required in the year of the change.

- Applying Form 8594 to stock sales. Unless a Section 338(h)(10) election applies, stock sales do not require this form.

- Missing the filing deadline. Per the form 8594 instructions, the form is due with the tax return for the year of sale, including valid extensions.

- Inadequate FMV documentation. The IRS expects each asset class allocation to be supportable with appraisals or documented fair market value analysis. Unsupported allocations are audit bait.

Each of these errors is avoidable with proper preparation — working with professional tax preparation services that specialize in business acquisitions significantly reduces the risk of audit exposure on all seven points above.

Frequently Asked Questions

What is Form 8594 used for?

Form 8594, the Asset Acquisition Statement Under Section 1060, is used to report how the purchase price from a business asset sale is allocated across seven defined asset classes. Both the buyer and the seller must attach it to their own federal income tax return for the year the sale occurred.

Who is required to file Form 8594?

Both the buyer and the seller in a qualifying asset acquisition must file Form 8594 separately, attaching it to their own federal return — whether a Form 1040, 1120, 1065, or 1120-S — for the tax year of the transaction.

Does Form 8594 apply to stock sales?

Generally no. Form 8594 is triggered by asset sales, not stock sales. The exception is a Section 338(h)(10) election, where a qualifying stock purchase is treated as an asset sale for federal tax purposes, requiring both parties to file Form 8594.

What happens if buyer and seller file inconsistent allocations?

Both parties must disclose the inconsistency on their Form 8594. The IRS may challenge either party’s allocation and recharacterize the purchase price across classes, potentially resulting in additional taxes, interest, and penalties.

When is Form 8594 due?

Form 8594 must be filed with the taxpayer’s federal income tax return for the year in which the sale occurred. If the taxpayer has a valid filing extension, the form is due by the extended deadline.

Here’s the Conclusion on IRS Form 8594

Form 8594 is a small form with significant financial consequences — getting the asset class allocations right protects both parties from audit risk and ensures each side’s tax position reflects the negotiated deal. Whether you’re the buyer building depreciation schedules or the seller managing capital gain exposure, these allocation decisions belong in the conversation well before closing day.

The allocation you negotiate today becomes the depreciation schedule and gain calculation that follows you for years. Working through a business sale or acquisition? Our team at Simplicity Financial has over 15 years of experience helping buyers and sellers navigate complex tax situations — including Form 8594 allocations that protect your bottom line. Contact us today for expert tax preparation support or explore our Tax Preparation Outsourcing services to get started.

Disclaimer: This content is for general informational purposes only and is not tax, legal, or financial advice. Tax rules and filing requirements can change, and the right approach depends on your specific situation. Please consult a qualified accountant, tax professional, or attorney before making decisions, and verify details with the IRS or relevant tax authorities.