When your W-2 never arrives—or your 1099-R is wrong—filing your return on time can feel impossible. Form 4852 is the IRS substitute form that lets you file an accurate return even when your employer or plan administrator fails to deliver proper wage or distribution documentation.

👀Missing a W-2 and the deadline’s getting loud? Get a clean filing plan in one call.

What Is Form 4852?

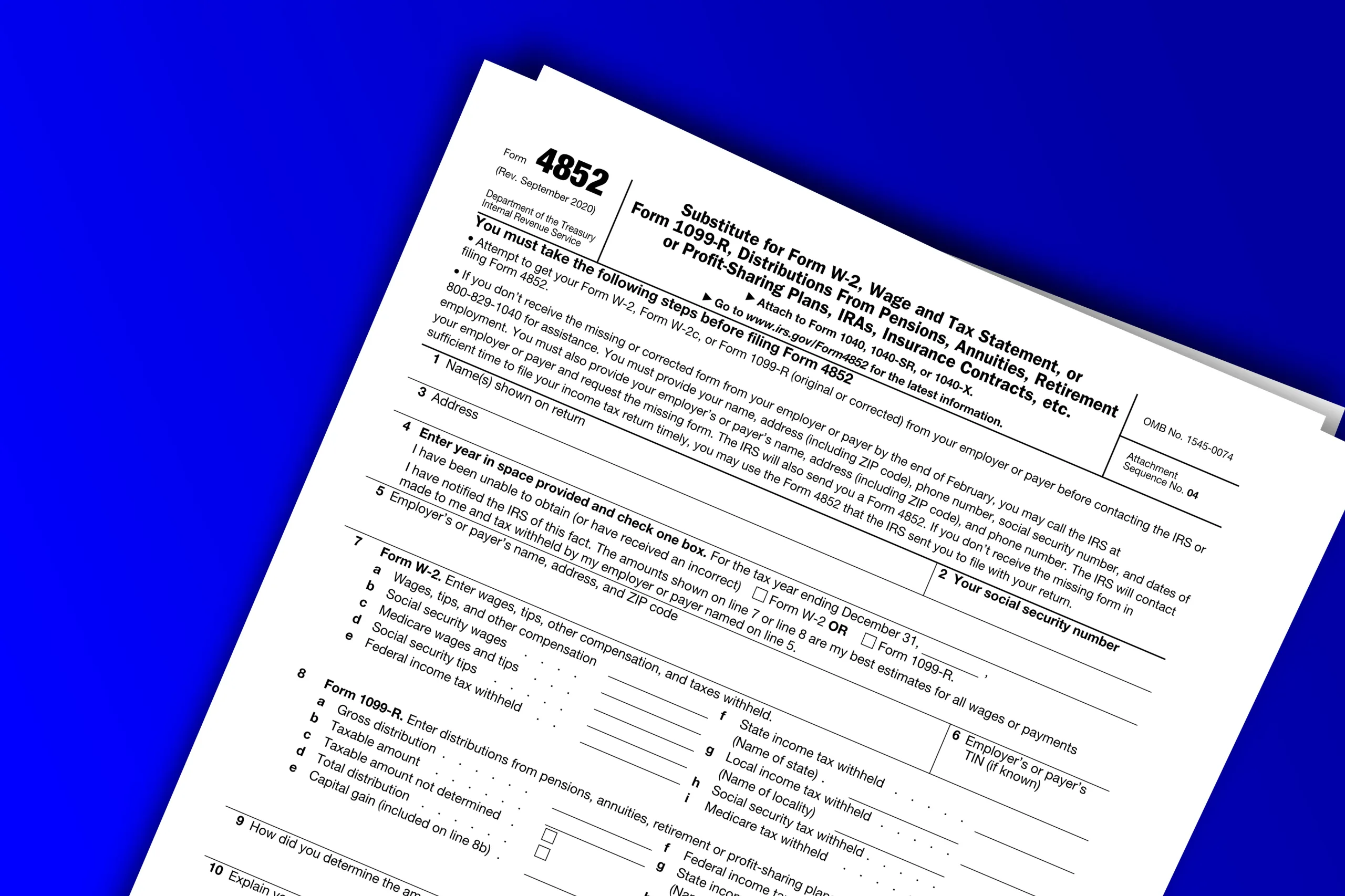

Tax form 4852 is an IRS substitute for Form W-2 or Form 1099-R, used when a taxpayer has not received—or has received an incorrect—wage statement or retirement distribution document by the filing deadline. The 4852 form exists so taxpayers are not penalized for an employer’s or payer’s failure to issue proper documentation. Think of it as a backup key: when your employer’s paperwork doesn’t show up, Form 4852 unlocks your ability to file on time. According to the IRS’s official page on Form 4852, it serves as a substitute for Forms W-2, W-2c, and 1099-R. The W-2 and 1099-R scenarios involve different form lines and tax consequences—both covered below.

Why You Might Need This Form: Common Reasons W-2s and 1099-Rs Go Missing

Missing tax documents are almost never the taxpayer’s fault. Common scenarios include an employer going out of business before issuing W-2s, payroll errors that sent documents to an outdated address, or independent contractor misclassification where wages were paid but no substitute for Form W-2 was issued. On the retirement side, custodians sometimes miss deadlines, leaving taxpayers without a substitute for Form 1099-R for pension or IRA distributions.

Regardless of cause, the filing deadline does not move. Taxes remain due by April 15, and this Form W-2 substitute is what protects your ability to file on time.

W-2 vs. 1099-R: Does the Type of Missing Form Change Anything?

Yes. A missing W-2 is typically an employer payroll issue with straightforward wage and withholding estimates. A missing 1099-R—covering distributions from pensions, IRAs, annuities, and profit-sharing plans—carries additional complexity: early distribution penalties (typically 10%), rollover rules, and variable withholding amounts make accurate estimation harder and any eventual amendment more consequential.

Steps to Take Before Filing Form 4852

Form 4852 instructions are clear: this form is a last resort, not a first option. Follow these steps in order.

Step 1: Contact your employer or plan administrator directly and request the missing document. Record the date and method of contact.

Step 2: If you still haven’t received the form by February 15, call the IRS at 1-800-829-1040. Have your full name, Social Security number, address, employer name and address, estimated wages and withholding, and employment dates ready. The IRS will contact the employer on your behalf.

Step 3: If the IRS cannot secure the form before your filing deadline, you may then use Form 4852.

Per IRS.gov’s guidance on Form 4852, completing these steps first is required. The April 15 deadline still applies—Form 4852 protects your on-time filing, not your right to delay it. Knowing what to do if you cannot get a W-2 from your employer ahead of time prevents last-minute scrambling.

How to Fill Out Form 4852

Knowing how to fill out Form 4852 without pay stub documentation is where most taxpayers hit a wall. Estimating wages without documentation requires careful recordkeeping and professional guidance to avoid accuracy-related penalties.

Here’s how to file this 4852 tax form correctly:

- Top section: Your name, address, Social Security number, and tax year

- Employer/payer section: Employer name, address, and EIN if known

- Line 7 entries: Wages, tips, compensation, federal income tax withheld, Social Security wages and taxes, and Medicare wages and taxes

If no pay stub is available, use bank deposit records to estimate gross wages; the IRS guide on reporting income on tax returns outlines acceptable estimation methods. The IRS recommends using your final pay stub if one is available.

Two limits to know: Social Security wages on Lines 7b and 7d cannot exceed the annual Social Security wage base. Medicare tax is 1.45% of all wages; high earners may also owe 0.9% Additional Medicare Tax.

All estimates must be made in good faith. Intentional misrepresentation carries serious consequences, including accuracy-related and civil fraud penalties. Keep your copy indefinitely—the IRS instructs taxpayers to retain Form 4852 until they begin receiving Social Security benefits. If you don’t do your own taxes, be sure to ask your certified tax accountant for a copy.

What Happens After You File—and When to Amend

After filing, the IRS verifies your Form 4852 amounts against employer payroll records. If you later receive the actual W-2 or 1099-R and the numbers match your estimates, no further action is needed. If the amounts differ—whether you’re still waiting on the document or your estimates were simply off—file Form 1040-X as soon as you receive the correct document.

Filing an amendment isn’t a red flag—it’s the expected process when estimates were used. Retain your Form 4852 copy for Social Security benefit verification long after the tax year closes.

Frequently Asked Questions

Is Form 4852 the same as a W-2?

No. Form 4852 is a substitute for Form W-2, not a replacement issued by your employer. It allows you to self-report estimated wage and withholding information when your employer fails to provide a W-2 by the deadline. The IRS may still verify reported amounts against employer records after you file.

What if I don’t have a pay stub to estimate my wages?

Bank deposit records are your best alternative. Add up employer deposits during the tax year to estimate gross wages. Employment contracts and offer letters can confirm your pay rate. For hourly workers with variable hours, the bank record approach is most reliable.

Filing with a missing W-2 doesn’t have to derail your tax season, but it requires following the right steps in the right order. Form 4852 is a legitimate IRS tool designed exactly for this situation, and using it correctly protects both your filing status and your refund timeline. For complex situations involving amended returns or IRS follow-up, professional tax preparation help can reduce both errors and stress.

Disclaimer: This content is for general informational purposes only and is not tax, legal, or financial advice. Tax rules and filing requirements can change, and the right approach depends on your specific situation. Please consult a qualified accountant, tax professional, or attorney before making decisions, and verify details with the IRS or relevant tax authorities.