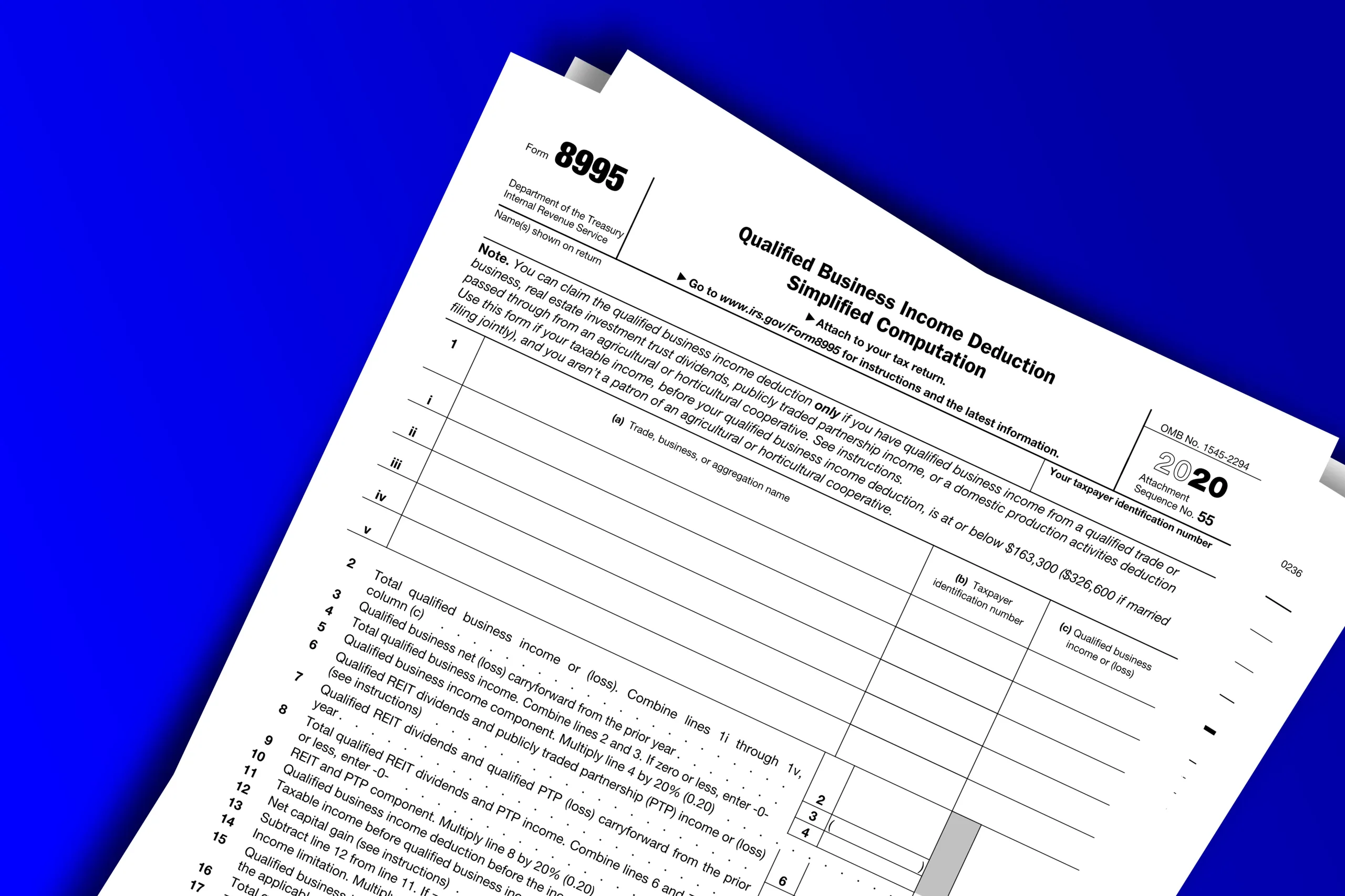

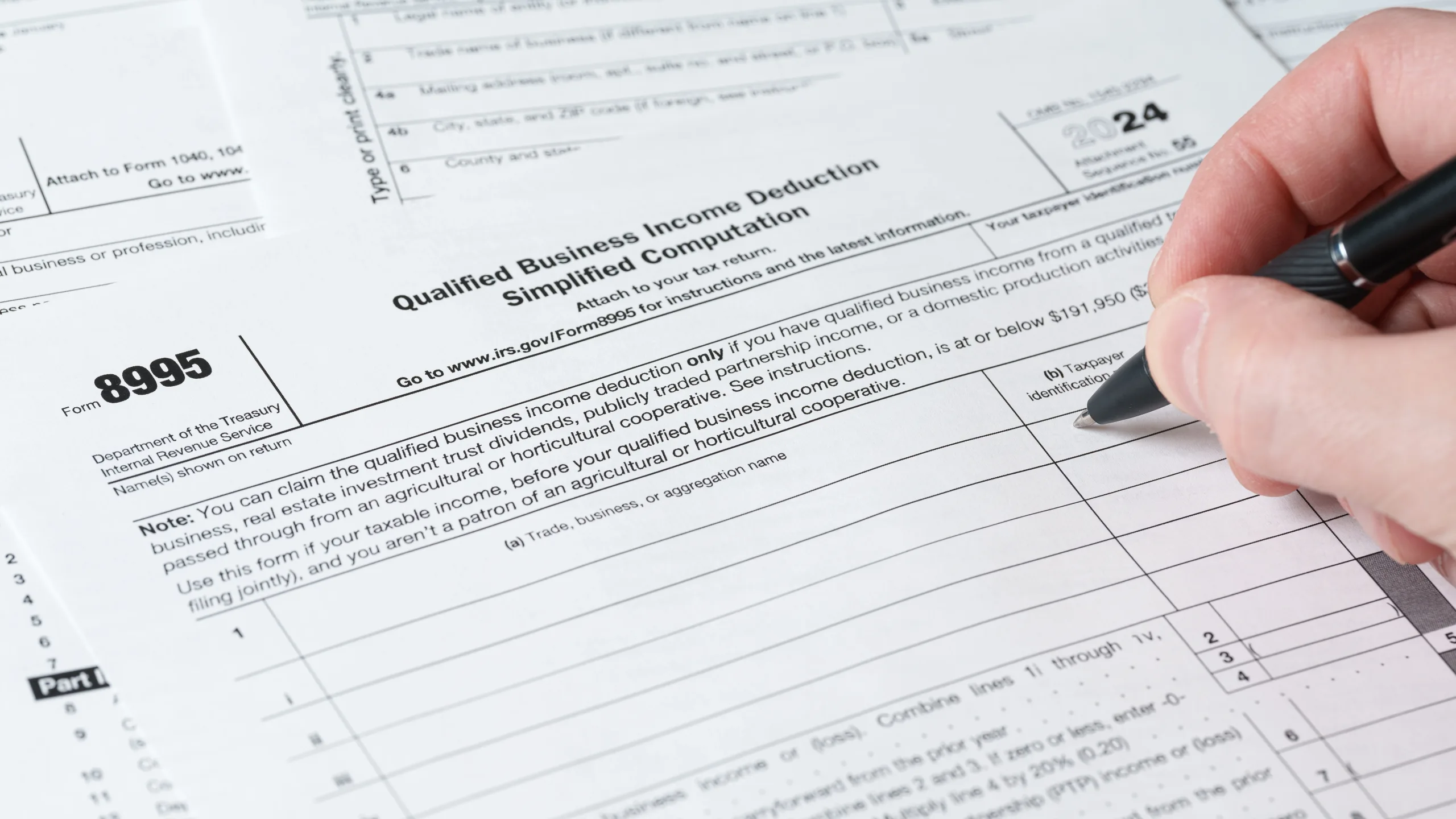

Form 8995 is where many pass-through business owners claim the Qualified Business Income (QBI) deduction. If you qualify, it can reduce taxable income in a meaningful way. If you do not qualify, forcing it can create a return that looks “off” in all the wrong places. The goal is to get the QBI deduction right, not to squeeze it in.

For a quick reality check: what is Form 8995? It’s the simplified form used to calculate the QBI deduction for certain taxpayers, while Form 8995-A is used in situations that require the more complex computation. The IRS confirms the purpose and how the forms are used on its page about Form 8995.

Simplicity Financial is a remote firm that helps business owners keep tax strategy practical and defensible, not theoretical. Learn more at Simplicity Financial, or if you want a QBI review that ties directly to your books and entity structure, start here: contact Simplicity Financial.

Form 8995 in One Sentence

The 8995 form calculates the QBI deduction for eligible business income, using rules that depend on your taxable income and the kind of business income you’re reporting.

That’s why the form feels “simple” only when your records are clean and your situation fits the simplified path. Otherwise, you may be looking at Form 8995-A and wondering why the math suddenly got serious.

Who Typically Uses Form 8995

Form 8995 is commonly used by owners of pass-through businesses, such as many sole proprietors, partnerships, S corporations, and LLCs taxed as pass-throughs. The “why” matters: QBI is generally about qualified income from qualified trades or businesses that flows through to your return.

This is also where business structure becomes more than paperwork. If you’re still deciding between entity options, the comparison in partnership vs LLC helps clarify how pass-through income typically flows and why it affects tax planning choices like QBI.

The Fast Filter: When Form 8995-A Shows Up

If Form 8995 is the “simple route,” then Form 8995-A is the “you need the full calculation” route. The IRS explains the details in the official Form 8995 instructions and the separate Form 8995-A instructions.

In plain English, the switch from Form 8995 to Form 8995 a is often tied to income levels and limitation rules. That doesn’t mean you did anything wrong. It means the deduction needs the more detailed computation.

If you want to understand the “who does not qualify” side at a deeper level, this guide on what business does not qualify for QBI deduction is a helpful companion read.

Qualified Business Income, Without the Fog

The QBI deduction is about qualified income from qualified business activity. Two practical points keep people out of trouble:

- QBI is not the same as gross revenue.

- QBI is not guaranteed just because you own a business.

This is where bookkeeping quality matters. If your income and expenses are mixed, uncategorized, or missing documentation, you can end up calculating a deduction on numbers that don’t hold up under basic review.

That’s why business owners who want QBI done correctly often benefit from systems support like outsourced bookkeeping services. When the books are clean, QBI becomes a calculation. When the books are messy, QBI becomes a debate.

A Table That Makes the Decision Easier

Here’s a quick table that helps you spot which form you’re likely dealing with, and what that implies for your prep work.

| Situation | Likely QBI form path | What to focus on |

| Straightforward pass-through income, no complex limitation factors | Form 8995 | Clean net income, accurate classifications, consistent records |

| Higher taxable income or limitation rules likely apply | Form 8995-A | W-2 wages, qualified property, detailed computations, continuity |

| Multiple business activities or multiple pass-through sources | Form 8995 or Form 8995-A | Tight documentation by activity, consistent reporting inputs |

| You’re not sure the business qualifies as a “qualified trade or business” | Start with eligibility review | Confirm the business type and limitation triggers |

This helps frame the phrase many owners search for: qualified business income deduction from Form 8995 or Form 8995-A. The deduction is one concept, but the form you use depends on your facts.

Form 8995 Instructions: The Inputs That Matter Most

The Form 8995 instructions matter because the form is only as accurate as the inputs you feed it. In practice, the most important inputs are:

- Qualified business income figures that match your business records

- Taxable income context that affects whether limitations apply

- Consistency across the return so the QBI story matches the overall tax story

If you want a better feel for how “one schedule affects another,” the guide on how to read tax returns can help you interpret your return as a connected document rather than isolated forms.

Form 8995-A Instructions: Why the Math Gets Heavier

The Form 8995-A instructions exist because the QBI deduction can be limited based on specific rules. In certain income ranges, the deduction becomes a more detailed computation, and additional components like W-2 wages and qualified property can matter.

The biggest mistake here is trying to “shortcut” the process. If your facts point to Form 8995-A, it’s worth doing the full calculation correctly rather than forcing the simplified route.

A good rule: if the deduction starts to feel like a negotiation, you probably need better documentation or a clearer strategy, not a faster calculator.

Entity Choices That Quietly Affect QBI Planning

A lot of QBI confusion starts upstream, with entity treatment. An LLC, for example, is a state law entity that can be taxed in different ways depending on elections and ownership. That’s why two LLC owners can have different tax outcomes.

If you want clarity on terminology, this guide on is an LLC incorporated or unincorporated can help you understand how LLCs are commonly treated and why elections matter.

If you made, or are considering making, an entity classification election, Form 8832 is often part of that decision. The election can change how income is treated and how tax planning fits together across the return, including how QBI strategy is approached.

Infographic-Friendly Section: The 5-Minute Form 8995 Prep Checklist

If you want Form 8995 to be smooth, your goal is to have a complete input pack before you open the form.

- Confirm the business type and whether QBI eligibility is likely

- Confirm you’re using net income that matches clean books

- Identify whether limitations are likely based on your overall taxable income

- Separate QBI-relevant activity from non-QBI activity in your records

- Keep a copy of how you calculated the inputs so the story is repeatable next year

This checklist is the difference between “we filed it once” and “we can file it cleanly every year.”

For many owners, this step becomes easier after a year-end cleanup and planning pass. That’s why the year-end tax planning checklist can be a useful routine if you want fewer surprises and better control.

Where Simplicity Financial Helps With Form 8995

For business owners, the QBI deduction often sits at the intersection of three practical needs: clean books, correct entity treatment, and accurate filing.

Simplicity Financial supports those needs in ways that fit real operations:

- When your biggest issue is messy records, outsourced bookkeeping services can help ensure QBI inputs are built on consistent categories instead of best guesses.

- When you want the filing handled end-to-end, tax preparation outsourcing can help you file confidently with the right supporting documentation.

- When QBI is part of bigger strategy decisions, like scaling payroll, adjusting owner compensation, or restructuring for growth, fractional CFO services can help connect tax decisions to the long-term plan.

If you want to keep learning, the Simplicity Financial blog includes additional tax planning topics written in plain language.

Form 8995: Next Steps With Simplicity Financial

Form 8995 is easiest when it’s treated like a calculation built on clean records, not a last-minute add-on. If you’re unsure whether you need Form 8995-A, or you want to confirm that your QBI deduction is defensible, a quick review can save time and prevent rework.

To get support remotely, start here: contact Simplicity Financial.

Frequently Asked Questions About Form 8995

What Is Form 8995 and Who Uses It

What is Form 8995? It’s used to calculate the QBI deduction for certain eligible taxpayers, typically involving qualifying pass-through business income.

8995 Form vs Form 8995-A: How Do You Know Which One Applies

The 8995 form is the simplified computation, while Form 8995-A is used when the deduction requires the more detailed calculation. The official Form 8995 instructions and Form 8995-A instructions explain when each applies.

What Does “Qualified Business Income Deduction From Form 8995 or Form 8995-A” Mean

It refers to the same deduction, but calculated through different forms depending on your facts. The deduction is the concept. The form is the method.

Where Can a Business Owner Get Help With Form 8995

If you want remote help with QBI planning and filing, Simplicity Financial supports U.S. business owners with bookkeeping, tax prep, and planning.

Disclaimer

This article is for general informational purposes only and does not constitute tax, legal, or accounting advice. Readers should consult a qualified accountant or tax professional for guidance tailored to their situation and verify details with official IRS resources before making decisions.