If you own a foreign business entity that the IRS treats as “not separate from you” for U.S. tax purposes, Form 8858 is the paperwork that makes that relationship official on your return. It’s how the IRS gets a clear picture of what the entity did, what it owns, and how money moved between the entity and you (or other related parties). In other words, Form 8858 is less about “filling out a form” and more about making your cross-border business story readable.

The IRS explains the purpose and reporting scope on its page about Form 8858. Using that framework, this guide breaks down who files, what records you need, which schedules matter most, and where people accidentally create headaches, especially when the entity is tied to a property, a side business, or a growing company abroad.

Simplicity Financial supports clients remotely across the U.S. through cross-border reporting and tax filing workflows. Learn more about the firm at Simplicity Financial, or start a conversation if you want your filing reviewed before it becomes a chain of rework: contact Simplicity Financial.

What Is Form 8858, in Plain English

People ask what is Form 8858 because the name doesn’t explain the problem it solves. Here’s the simplest explanation:

Form 8858 reports activity of certain foreign “disregarded entities” and certain foreign branches (qualified business units) owned by U.S. persons. It tells the IRS what the entity/branch did financially and how it connects to your U.S. return.

A quick “real-life” example:

A U.S. person owns a single-member company in another country. The company receives rent, pays expenses, and holds a bank account abroad. For U.S. tax purposes, it may be treated as a disregarded entity. Disregarded entity Form 8858 reporting is how you show the activity clearly rather than leaving the IRS to guess from scattered forms.

Form 8858 Filing Requirements: Who Typically Has to File

Form 8858 (Schedule M) papers. Transactions Between Foreign Disregarded Entity (FDE) or Foreign Branch (FB) and the Filer or Other Related Entities. Form 8858 (Schedule M) documentation published IRS USA 09.30.2021. American tax document on colored

The phrase Form 8858 filing requirements can sound intimidating, but it boils down to one question: does a U.S. person own a foreign disregarded entity or operate a foreign branch that triggers reporting?

The official rule set is detailed in the Form 8858 instructions. In practice, filers commonly include:

- Individuals with a foreign disregarded entity used for business activity or holding income-producing assets

- U.S. owners of entities that are treated as disregarded for U.S. tax purposes (even if the entity is recognized as separate under foreign law)

- Taxpayers with foreign branches that function as a qualified business unit

If you’re juggling multiple international forms, it helps to know that these filings often come as a “set.” A business owner dealing with Form 8858 may also have other cross-border reporting, depending on the facts. If you need those related guides:

- Form 5471 is common when a foreign corporation is involved

- Form 3520 can apply in foreign gift/trust situations

- Form 3520-A can come into play for foreign trust annual reporting

8858 Form: What You’re Actually Reporting

An 8858 form is not just “income.” It’s a structured snapshot of the entity’s activity.

Most filings are trying to answer:

- What does the foreign entity or branch own?

- What did it earn and spend?

- How did money move between it and the U.S. owner (or other related parties)?

- Are the records consistent with what’s reported on the U.S. return?

This is why people get stuck. The form requires you to translate foreign activity into a U.S. reporting format. You don’t need a dramatic strategy. You need good source records.

If you want a simple way to understand where numbers land once they’re reported, the guide on how to read tax returns helps you interpret the “final story” your return is telling.

Form 8858 for Foreign Rental Property: A Common Scenario

One of the most frequent searches is Form 8858 for foreign rental property, because property ownership is where “simple investment” can quietly become “international reporting.”

Example:

A U.S. person owns a foreign single-member entity that holds a rental condo abroad. The entity collects rent, pays local expenses, and may even hold a mortgage. Even if the rental feels straightforward, the IRS may still expect reporting through Form 8858 if the setup meets the reporting rules.

In this scenario, the most important habit is documentation:

- rental income statements

- expense receipts and invoices

- bank activity (especially if accounts are abroad)

- proof of ownership and entity status

- any related-party transfers (for example, the U.S. owner funding repairs)

When records are incomplete, the filing becomes stressful. When records are clean, the filing becomes a structured translation exercise.

This is one reason some clients choose outsourced bookkeeping services even when the “business” feels small. The goal isn’t fancy reporting. It’s keeping the paper trail consistent enough that the filing doesn’t turn into a reconstruction project.

Instructions for Form 8858: The Records You Should Gather First

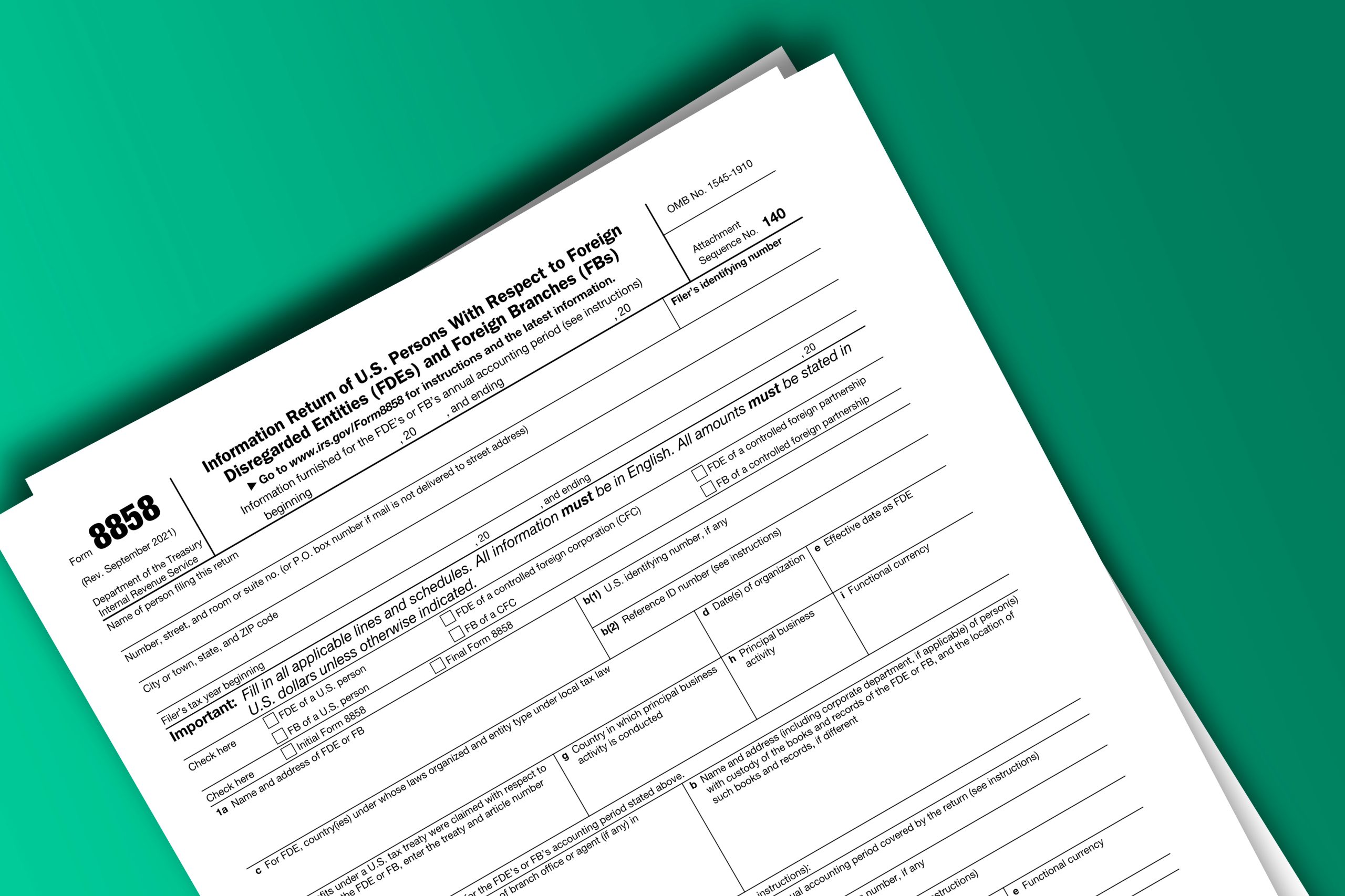

Form 8858 papers. Information Return of U.S. Persons With Respect to Foreign Disregarded Entities (FDEs) and Foreign Branches (FBs). Form 8858 documentation published IRS USA 09.30.2021. American tax document on colored

Before you start any Form 8858 filing instructions, build a single folder with the core records. This reduces errors and makes review easier if anything is questioned later.

A practical document pack:

- Entity ownership details and basic formation documents

- Year-end balance sheet and profit/loss for the entity or branch (or a consistent ledger)

- Bank statements for accounts connected to the entity

- Related-party transaction detail (owner contributions, reimbursements, loans, distributions)

- Foreign tax statements or summaries if applicable

The IRS gives the technical structure in the instructions form 8858. The difference between a smooth filing and a messy one is whether you can support the numbers with a clear trail.

Form 8858 Schedule M: The Section That Causes the Most Cleanup

Form 8858 Schedule M is where you disclose transactions between the foreign disregarded entity/branch and related parties. It’s not reserved for suspicious activity. It’s where routine real-world flows become reportable because they involve related parties.

Common items that land in Schedule M:

- Owner funding the entity (capital contributions)

- Owner reimbursing expenses (or the entity paying the owner back)

- Management fees paid to a related U.S. entity

- Loans, interest, repayments between related parties

- Payments for services, rent, or shared expenses between related entities

Example:

A U.S. owner pays the foreign entity’s insurance and repairs personally, then records it as a reimbursement. Or the owner deposits funds into the foreign entity’s bank account to cover a gap between rent payments. Those are normal actions, but they create related-party flows that often need to be tracked cleanly for Form 8858 schedule m reporting. People also search Form 8858 sch m for the same reason: they’re trying to figure out whether “routine money movement” counts. It does, if it’s between related parties and required by your filing scenario.

The clean way to make Schedule M workable is to track related-party transactions as their own category throughout the year, rather than trying to rebuild them from memory.

Forms 8858: When You Might Need More Than One

People search forms 8858 (plural) because one return can require multiple filings.

You may need more than one Form 8858 if you have:

- multiple foreign disregarded entities, each with its own activity and accounts

- a foreign branch and a foreign disregarded entity

- separate entities that each meet reporting requirements

The key is not the number of forms. The key is consistency: each form should reconcile to the records for that entity/branch, and your return should tell one coherent story.

Form 8858 Instructions: Where People Get Stuck

Most problems aren’t caused by people “not trying.” They’re caused by one of these:

- Treating foreign bookkeeping formats as if they automatically match U.S. reporting expectations

- Missing related-party details (Schedule M is often where the gaps show up)

- Mixing personal and entity expenses without documentation

- Not keeping consistent year-end statements

- Filing without a clear record of the entity’s functional activity

If you feel your situation is becoming complex, it helps to separate two things: compliance reporting and the fear of “audit” in the abstract. This explanation of audit vs tax accounting helps clarify what you’re actually doing here: filing correctly with supportable records.

How Simplicity Financial Helps With Form 8858 Workflows

Form 8858 Information Return of U.S. Persons With Respect to Foreign Disregarded Entities (FDEs) and Foreign Branches (FBs) phrase on the page.

A good Form 8858 filing isn’t “more words.” It’s better structure. Simplicity Financial supports remote clients by making the workflow repeatable:

- Ensuring records are organized before numbers are reported

- Reconciling entity activity to the U.S. return so filings are consistent

- Reducing rework by building a clear document pack and review process

For ongoing support across entities, banks, and reporting requirements, remote accounting services can be a practical fit for owners who don’t want international compliance to become a seasonal crisis.

If you want the filing handled end-to-end with a coordinated process, tax preparation outsourcing is often the simplest route when multiple forms and schedules are in play.

For additional tax topics and compliance guides, visit the Simplicity Financial blog.

Form 8858: Next Steps With Simplicity Financial

If you’re filing Form 8858, the goal is to make the foreign entity or branch understandable on a U.S. return: clean records, clear related-party flows, and schedules that match your situation. When the document pack is complete, the form becomes a structured translation. When it isn’t, the form becomes guesswork.

If you want a remote review of your Form 8858 filing requirements and the supporting records before you submit, reach out here: contact Simplicity Financial.

Frequently Asked Questions About Form 8858

What Is Form 8858 Used For

What is Form 8858? It’s used to report activity of certain foreign disregarded entities and foreign branches owned by U.S. persons, as described in the IRS guidance on the form.

Where Can Someone Find Form 8858 Instructions

The IRS provides the official Form 8858 instructions, which outline who files, what to include, and how to complete required schedules.

What Are the Most Common Form 8858 Filing Requirements

Form 8858 filing requirements commonly apply when a U.S. person owns a foreign disregarded entity or operates a foreign branch that triggers reporting, depending on the facts and filer category described in IRS guidance.

When Does Form 8858 Schedule M Matter

Form 8858 schedule m matters when there are transactions between the foreign entity/branch and related parties, such as owner contributions, reimbursements, fees, or intercompany payments.

Does Form 8858 Apply to Foreign Rental Property

Form 8858 for foreign rental property can apply when the rental is owned through a foreign disregarded entity or foreign branch structure that triggers reporting, especially when there are separate accounts and related-party funding flows.

Where Can Someone Get Help With Form 8858 Reporting

For remote help with Form 8858 and related international reporting, Simplicity Financial supports clients across the U.S.

Disclaimer

This article is for general informational purposes only and does not constitute legal, tax, or accounting advice. Readers should consult a qualified accountant or tax professional for guidance tailored to their situation and verify details with official IRS guidance before making decisions.