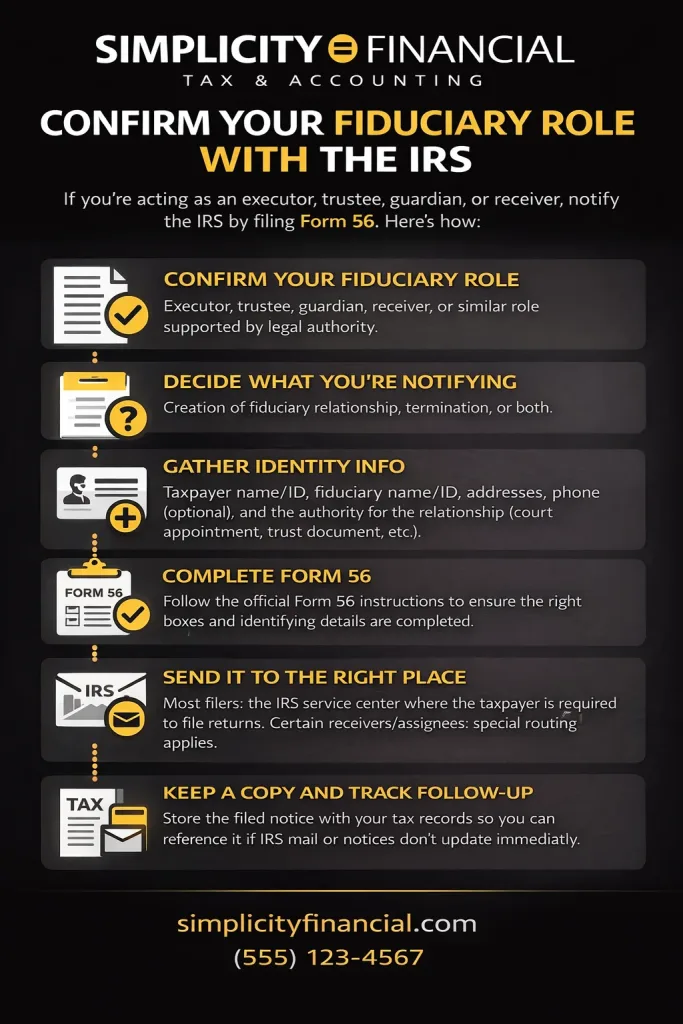

Form 56 is the IRS notice that tells the government, “A fiduciary is now the point person for this taxpayer.” If you’re acting as an executor, trustee, guardian, conservator, receiver, or similar role, filing Form 56 can help the IRS send the right notices to the right person and recognize your authority to handle tax matters.

Simplicity Financial supports clients remotely across the U.S. and helps families and business owners keep complex tax matters organized, especially when life events create new filing responsibilities.

The quick answer that most people are looking for immediately is:

- File Form 56 when a fiduciary relationship is created or terminated.

- Use it to notify the IRS under the rules described on the IRS page about Form 56 and the official Form 56 instructions which can be found here.

- In most cases, you file it with the IRS service center where the person you’re acting for is required to file tax returns, with special routing rules for certain receiverships and assignments.

What Form 56 Does in Plain English

Form 56 is called “Notice Concerning Fiduciary Relationship.” You use it to notify the IRS of the creation or termination of a fiduciary relationship, and (in certain situations) to give notice of qualification under other tax rules.

This form does not “transfer assets,” “close an estate,” or “file the tax return for you.” It simply tells the IRS who is authorized to act and where IRS correspondence should go.

If you’re reading IRS letters and thinking, “They should be talking to me, not the deceased person,” Form 56 is often part of making that communication line clearer.

Who Files Form 56

When people ask who needs Form 56, it usually comes down to whether you are legally acting on someone else’s behalf for tax matters. Here’s a table you can use as a quick reference.

| Role | Common situation | Why Form 56 matters |

| Executor/administrator | Handling a decedent’s final return and estate matters | Establishes you as the IRS contact for the decedent/estate |

| Trustee | Managing trust tax matters | Shows you’re the fiduciary who can receive IRS notices |

| Guardian/conservator | Managing an incapacitated person’s affairs | Signals fiduciary authority for tax communications |

| Receiver/assignee | Receivership or assignment for benefit of creditors | Special filing timing and routing rules apply |

| Fiduciary for a terminating entity | Entity is terminating but needs a fiduciary to handle tax matters | Allows fiduciary representation after termination |

If your role sounds right but you’re unsure whether the IRS needs a notice, the official instructions for IRS Form 56 spell out the filing purpose and who should file.

Form 56 Instructions: When to File

The official Form 56 instructions are clear about timing in broad terms: you generally file Form 56 when you create or terminate a fiduciary relationship.

Practical examples of “created”:

- A court appoints you executor of an estate.

- You become a trustee and begin acting for the trust.

- You are appointed guardian or conservator for an individual.

Practical examples of “terminated”:

- Your fiduciary role ends and a successor takes over.

- The fiduciary relationship is otherwise terminated under your legal authority.

Special timing note: the instructions also describe an accelerated timeline and special routing for certain receiverships and assignments for the benefit of creditors, including filing within a set window and sending to an IRS Advisory office.

Where to Send Form 56

This is one of the most searched phrases for a reason: you can fill out Form 56 perfectly and still slow things down if it’s mailed to the wrong place.

Here’s the simplest, most accurate rule from the IRS instructions form 56:

- In general, file Form 56 with the IRS service center where the person you are acting for is required to file tax returns.

And here’s the important exception the instructions highlight:

- Certain receivers and assignees (in non-bankruptcy proceedings) have a separate submission route to an IRS Advisory office, and may also file a separate Form 56 with the service center to satisfy notice requirements.

So when someone asks where to send Form 56, the real answer is: it depends on the type of fiduciary role, but most filers send it to the IRS service center tied to the taxpayer’s filing location.

Form 56 Filing Flow in 6 Steps

Form 56 Filing Steps That Prevent Delays

Form 56 is easiest when you prepare first. Start by confirming your fiduciary role and the document that grants authority, then decide whether you’re notifying the IRS of a new fiduciary relationship, a termination, or another change. Next, gather the names, identifying details, and addresses for both the taxpayer and the fiduciary so the form matches IRS records exactly.

Once the form is complete, file it to the correct IRS destination. Most filers send it to the IRS service center tied to where the taxpayer is required to file. Some situations have different routing requirements, so it’s worth checking the instructions before sending. Finally, keep a dated copy of the filed notice and submission proof so you can reference it if mail or IRS notices don’t update immediately.

Form 56: The Parts People Usually Get Wrong

Most mistakes are not “hard tax law” mistakes. They’re paperwork mismatches.

Common issues the Form 56 instructions warn about, or that commonly create delays:

- Filing the form for the wrong person or entity (one Form 56 per person you’re acting for).

- Forgetting to file separate notices when multiple fiduciaries exist (the instructions note separate filings or notice).

- Sending it to the wrong IRS destination when special routing applies (receivers/assignees).

- Not keeping proof of what was sent and when.

If you’re handling multiple filings at once and the paperwork is starting to blur, the guide on how to read tax returns can help you keep forms, roles, and responsibilities straight.

When You Might Need More Than One Form 56

This surprises people, so it’s worth stating clearly.

You may need multiple Form 56 filings when you are acting in different fiduciary capacities for different “persons” in IRS terms. A common example is someone serving as fiduciary for both a decedent and a related trust. The instructions emphasize filing a separate Form 56 for each person for whom you are acting.

The key is to match the form to the taxpayer/entity the IRS is tracking.

How Simplicity Financial Helps With Fiduciary Tax Work

Fiduciary tax work tends to be emotionally loaded and deadline-heavy at the same time. People are grieving, managing paperwork, or stepping into responsibility for the first time. The value of a good process is that it removes uncertainty.

Simplicity Financial supports remote clients with:

- Tax preparation outsourcing for accurate filing support when there are multiple moving pieces

- Outsourced bookkeeping services when records need to be organized before filings can be completed cleanly

- Fractional CFO services for situations where fiduciary duties intersect with business operations, ongoing reporting, or complex financial planning

For more plain-English tax guides, visit the blog.

Form 56: Next Steps With Simplicity Financial

If you’re filing Form 56, the goal is simple: get the IRS communicating with the right person, using the right authority, as early as possible. Use the official Form 56 instructions to complete it correctly, send it to the right destination, and keep a copy with your records.

If you want a remote professional to help you confirm timing, reduce mistakes, and coordinate the filing alongside any related tax work, start here: contact Simplicity Financial.

Frequently Asked Questions About Form 56

Form 56 Instructions: What is this form actually for

The IRS explains that Form 56 can be used to notify the IRS of the creation or termination of a fiduciary relationship and for certain qualification notices.

Instructions Form 56: When should a fiduciary file it

The instructions form 56 state that, generally, you file Form 56 when you create or terminate a fiduciary relationship.

Instructions for IRS Form 56: Where to send Form 56

In general, the instructions for IRS Form 56 say to file Form 56 with the IRS service center where the person you’re acting for is required to file returns, with special routing for certain receivers and assignees.

Where to send Form 56 if you are the executor of an estate

Most executors file Form 56 with the IRS service center tied to where the decedent’s returns are filed, following the “where to send Form 56” rule in the instructions.

Where can someone get help with Form 56 and related filings

For remote help coordinating fiduciary notices and related tax filings, Simplicity Financial supports clients across the U.S.

Disclaimer

This article is for general informational purposes only and does not constitute legal, tax, or accounting advice. Readers should consult a qualified professional for guidance tailored to their situation and verify details with official IRS guidance before making decisions.